Even shitcoins want suit and tie

-

Many believe that an ETF guarantees the price increase of the cryptocurrency, but it is not.

-

Ethereum’s case is key: a “serious” and useful cryptocurrency is not driven by its ETF.

Fever by ETFs in cash in the United States shows no signs of deceleration. More and more companies submit applications to the stock and securities commission (SEC) to issue these financial instruments that seek to take cryptocurrencies to the traditional market.

From consolidated projects to Memecoins and Shitcoins without apparent utility, everyone wants a place in US bags. But what real value is an ETF to a cryptocurrency? Many believe that it guarantees a price increase, but the reality is more complex.

Ether’s case (eth), native Ethereum currency, demonstrates it: even a cryptocurrency with a solid proposal does not necessarily benefit from its ETF.

A parade of varied proposals

The panorama of cryptocurrency ETFs in the United States reflects the diversity of the market: A mosaic of serious, speculative and frankly extravagant projects.

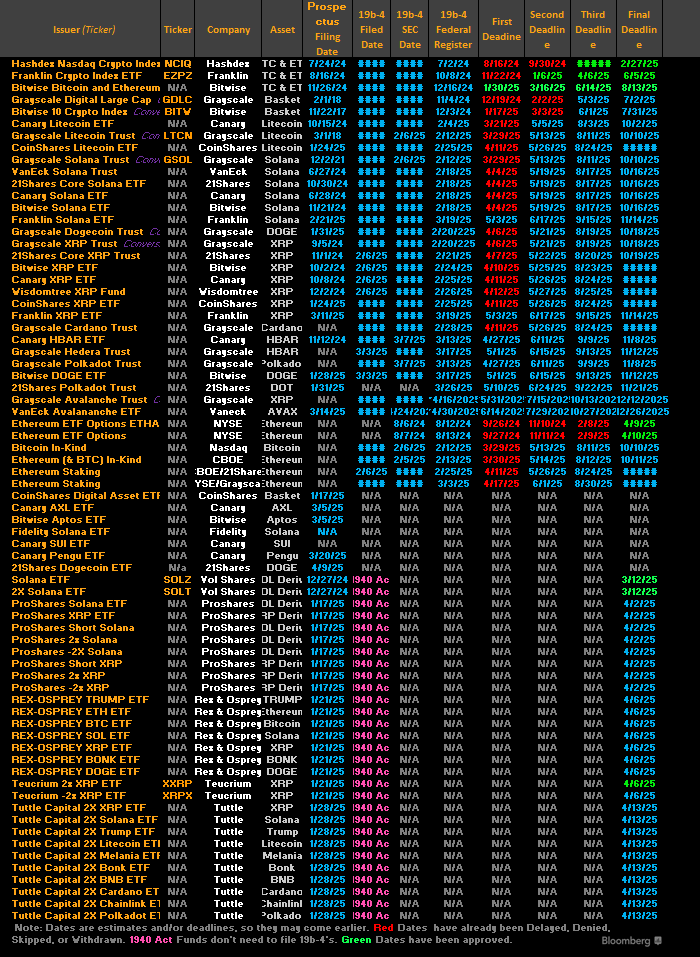

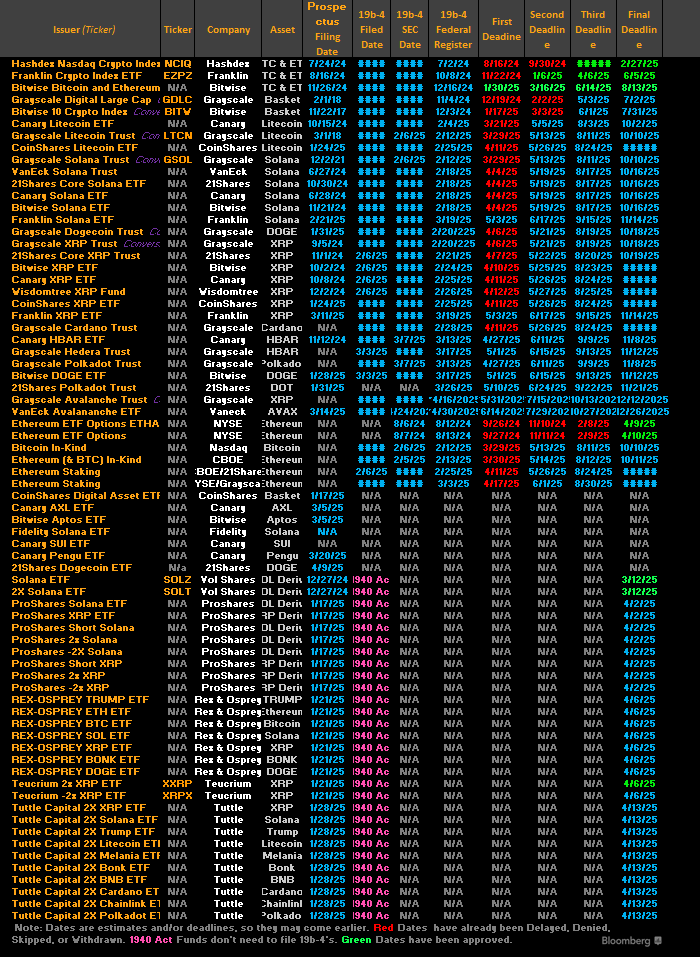

As Cryptonoticias reported on April 22, until that moment, the SEC had received 72 applications for funds based on a wide range of cryptoactive.

Among them, we find names like Solana (Sol), BNB, XRP, Cardano (ADA), Litecoin (LTC) and Polkadot (DOT). However, there are also surprising proposals, such as Memecoins such as Dogecoin (Doge), Bonk (Bonk) and even Pengu (Pengu).

Other projects, such as Hedera (Hbar), Aptos (APT), Avalanche (Avax), Axlar (Axl), Chainlink (Link), Sui (SUI) and SEI, complete this heterogeneous list.

This week, several of these requests faced delays. James Seyffart, ETF specialist at Bloomberg Intelligence, reported that The sec He postponed decisions about the figure of ETF Stking of Ethereum and the ETF of Dogecoin.

“I anticipate more delays today, or at least this week, in some presentations of ETF of Solana and Hbar,” said the specialist.

In your opinion, this is predictable. “The final deadline for most of these procedures is October 2025 or later,” said Seyffart. “It is possible that the SEC does not take so long to make its decision, but much will depend on how actively they get involved in applications,” he added.

For her part, the journalist Eleanor Terrett reported that the SEC postponed until June 17 the decision about the XRP ETF presented by Franklin Templeton.

While some proposals stagnate, others continue to emerge. Yesterday, the Swiss Asset Manager 21 presented a registration form S-1 for an ETF based on sui (SUI) before the SEC.

In addition, on April 30, the Canary Capital investment firm presented a leaflet for an ETF of SEI with Staking, adding to the wave of applications.

This constant flow of proposals reflects market enthusiasm, but also raises questions about the viability and usefulness of these funds.

The precedent of the Bitcoin and Ethereum ETF

To understand the phenomenon of ETFs, it is useful to look at the cases of Bitcoin (BTC) and Ethher (ETH), the pioneers in this field.

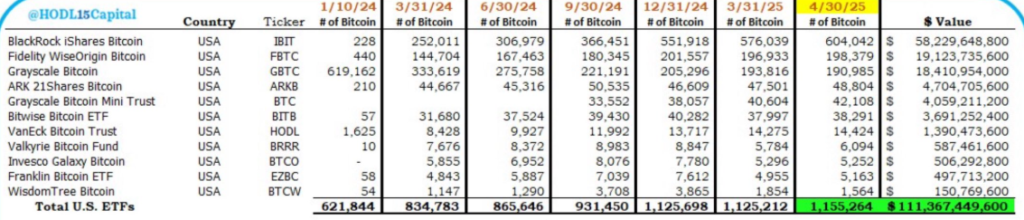

The Bitcoin Cash ETFs began quoting in January 2024 and quickly became a resounding success. In just 15 months, these funds have accumulated 1,155,814 BTC, equivalent to $ 128,000 million, representing 6.4% of all BTC in circulation. Only in April 2025, Bitcoin ETF holdings grew by 32,521 BTC.

The success of the Bitcoin ETF is largely due to the unique characteristics of this currency, which make it an attractive long -term reserve. The main is its shortage: Bitcoin’s supply is limited to a maximum of 21 million BTC, a stop that will never be overcome.

This characteristic, combined with its resistance to censorship and its unconfiscable nature, makes Bitcoin especially attractive in economic or political crisis scenarios.

Unlike cryptocurrencies, which often depend on cases for technical or speculative use, Bitcoin offers a clear value proposal as a decentralized and safe asset.

These qualities have promoted the confidence of institutional investors, who see in Bitcoin’s funds an accessible way to expose themselves to this asset.

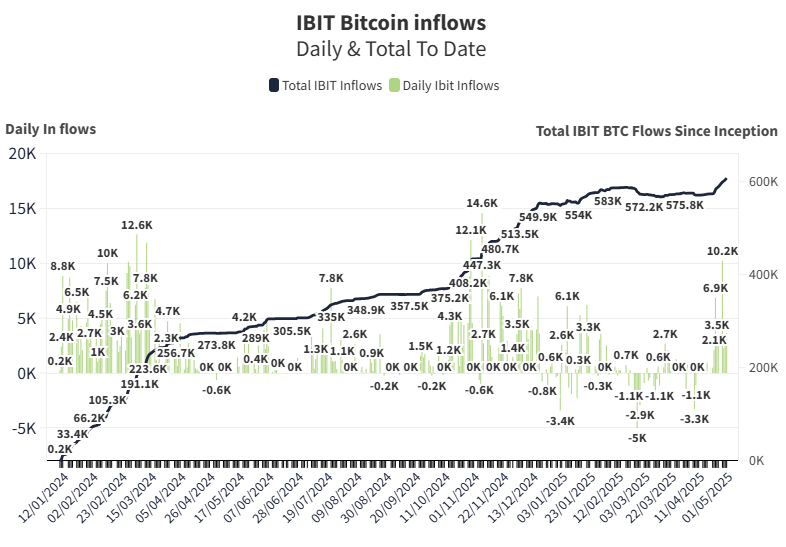

The most prominent background is the Ishares Bitcoin Trust (Ibit) of Blackrock. In just five months since its launch, it became the largest Bitcoin background in the world, with 288,670 BTC.

For the end of April 2025, it already had more than 600,000 BTC. This success demonstrates the appetite of investors by Bitcoin and the ability of ETFs to channel large capital flows.

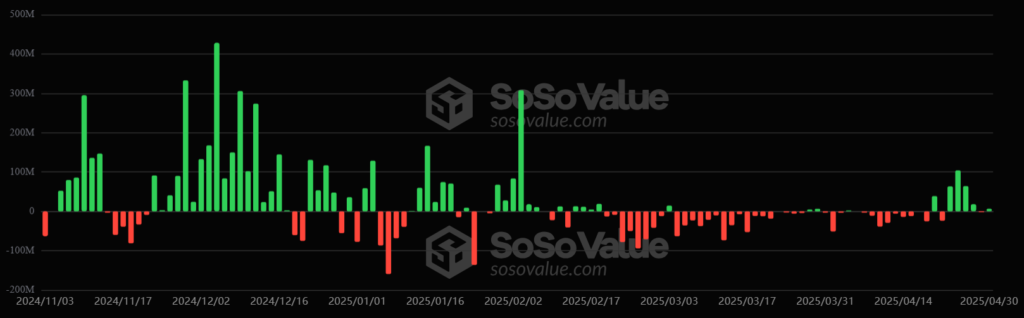

In contrast, the ETF of Ethereum, launched in June 2024, have had much more modest performance. Since their debut, they have registered money tickets for 2,490 million dollars, a significantly lower figure compared to Bitcoin funds.

This shows an uncomfortable truth. Having an ETF does not guarantee the success of a cryptocurrency, even if it’s eththe second cryptocurrency for market capitalization and a platform with a clear value proposal, such as intelligent contracts and decentralized finances (DEFI).

The ETF myth as a price engine

A common mistake among cryptocurrency enthusiasts is to assume that an ETF automatically triggers the price of a digital asset.

Logic seems simple: an ETF facilitates investment by allowing traditional investors to access a cryptocurrency without managing Wallets or Exchange.

This, in theory, increases demand and, therefore, the price. However, reality is more nuanced.

An ETF gives exposure to institutional investors and expands adoption through fund managers. If the fund is successful, it can generate an upward impulse in the quote of the underlying asset.

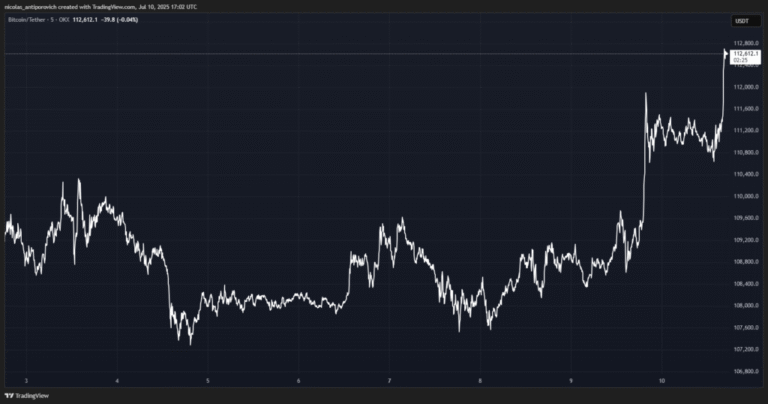

But Ethereum’s case shows that this does not always happen. Despite having ETF, the price of ETH has not only experienced a great increase, but has fallen, as can be seen in the image below:

If a cryptocurrency with such a robust utility as Ethereum does not benefit from your ETF, what hope does cryptocurrencies of zero or doubtful utility (that is, shitcoins) have?

It is worth clarifying that “shitcoins” (shit coins, in English), is a term used to refer to cryptocurrencies with little or no real -use, utility or purpose. They are considered “junk coins” due to their low quality, often created for purely speculative purposes and without a solid technical or economic basis.

The ETF is not a magical wand. Facilitates investment, but does not guarantee that investors are launched to buy.

As Eric Balchunas, Bloomberg specialist points out, ETFs make adoption easier for the general public. However, that does not automatically amounts to a price increase.

Investors evaluate factors such as project utility, market confidence and general economic conditions before compromising their capital.

Who wins with the ETFs?

If the ETF do not ensure a price increase, Why do so many companies rush to launch them? The answer is in management commissions.

Fund managers, such as Blackrock, Franklin Templeton or Canary Capital, generate income through the rates they charge for administering these financial instruments.

They don’t care if the price of cryptocurrency rises or low; Its gain depends on the volume of transactions and the interest of investors in negotiating the ETF actions.

This dynamic explains why we see ETF proposals for such disparate cryptocurrencies, from supposedly serious projects such as Solana and Litecoin to Memecoins such as Pengu or even Shitcoins of doubtful reputation.

Balchunas and Seyffart predict that the ETFs of Solana and Litecoin have a 90% chance of approved, with limit dates for the verdict of the SEC in October of this year.

Managers do not necessarily bet on the intrinsic value of these assets; Its objective is to capture the attention of investors, especially in a market where cryptocurrencies, even the most speculative, generate excessive enthusiasm.

In this sense, ETFs become a vehicle to monetize fever on cryptocurrencies, regardless of the usefulness of underlying projects.

The risk of suit and tie shitcoins

The ETF proliferation for Shitcoins raises a risk for investors since they lack a solid value proposal.

Memecoins, for example, depend on speculation, support for celebrities or viral fashions on social networks, but at the fundamental or technological level they have nothing to support them. It is pure and hard speculation.

An ETF can give them an air of legitimacy when presenting them as a regulated investment option, but this does not change their volatile and risky nature.

Imagine a scenario in which an ETF a little known Shitcoin until then attracts institutional investors, attracted by novelty or media hype.

If the fund fails to generate sustained interest, investors could face significant losses. Worse, the fact that the price of one of these ETF collapses could damage the perception of cryptocurrency ETFs in general, even affecting the funds based on more solid projects.

Cryptocurrency ETF fever is a reflection of the current market moment: a space where Innovation coexists with uncontrolled speculation. Investors must look beyond the suit and tie that an ETF gives to a cryptocurrency. The real question is not whether an asset has an ETF, but if it offers a real value proposal.

Discharge of responsibility: The views and opinions expressed in this article belong to its author and do not necessarily reflect those of cryptootics. The author’s opinion is informatively and under no circumstances constitutes an investment recommendation or financial advice.