How do you explain that more than 60 banks are on the brink of collapse in the United States?

Key facts:

-

When a bank collapses, a series of events can affect the system as a whole.

-

For the economy, the effects can be far-reaching.

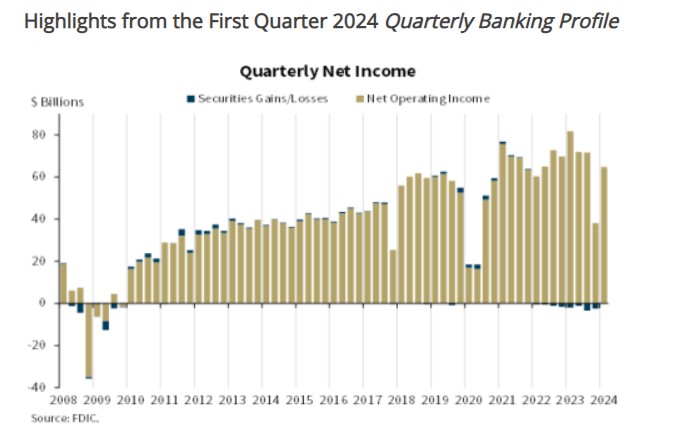

The quarterly report of the Federal Deposit Insurance Corporation (FDIC) last week revealed a series of problems facing the US banking sector. On the one hand, it points out that 63 banks were on the verge of insolvency during the first quarter of 2024. This compared to 52 financial entities included in the “list of problematic banks” during the third quarter of 2023.

On the other hand, the report also showed that Banks collectively accumulate unrealized losses worth $517 billion, an increase of $39 billion from the previous quarter. And not satisfied with that poor forecast for the financial health of banks, the FDIC added: “this is the ninth consecutive quarter of unusually high unrealized losses since the Federal Reserve began raising interest rates in the first quarter of 2022. ».

All of this data can be received by anyone like lightning in the middle of a storm, although the weather can become even more complicated to give way to a hurricane. This is taking into account that the Bank Term Financing Program (BTFP), created by the Federal Reserve to stop the spread of contagion due to financial collapses, stopped accepting new loan applications last March.

So the current complicated banking landscape brings to mind last year’s crisis when, in just two months, regional banks Signature, Silvergate and Silicon Valley failed. Are Financial institutions collapsed as customers flocked to withdraw their deposits. Many of them were technology or cryptocurrency companies that needed money to cover losses and because better savings rates were available elsewhere.

All of this hurt banks’ profitability at a time when high interest rates had already weakened their balance sheets by reducing the value of their government bond holdings. Silvergate failed first, but the collapse of Silicon Valley Bank on March 10 was particularly memorable. He triggered a bank run by announcing he needed to raise capital after being forced to sell bonds at a loss.

After those events, banks have had another year to adjust to higher interest rates, plus they can still borrow from the Federal Reserve through another facility called the discount window. However, it is likely that the closure of the BTFP increase banks’ borrowing costs, which means your profit margins will fall. They could react with higher interest rates or making less credit available to customers, which would have a direct impact and weaken the economy.

Ultimately, all of the above could combine and create the perfect whirlwind with a second foreseeable change that would create new dangers for the sector. It’s something that has happened before, as happened during the 2008 financial crisis.

Now the factors that gave rise to past crises would be combining again and there are at least 3 signs that prove it:

1- Loans + default = collapse

Before: In the years leading up to the 2008 crisis, there was a boom in the housing market in the United States, characterized by a rapid increase in property prices. Banks gave subprime mortgage loans to people who couldn’t pay them, causing a housing bubble that eventually burst.

Now: Economic turbulence, including rising interest rates and possible recessions, could lead businesses and individuals to struggle with payments.

For example, if a significant portion of commercial real estate loans default due to declining property values, Banks that invested heavily in this sector could face substantial losses. Similarly, an increase in consumer loan delinquencies, such as credit card debt, could erode banks’ profitability.

2- The inevitable massive contagion

Before: Collapse of large financial institutions: In September 2008, the bankruptcy of Lehman Brothers, one of the main investment banks in the United States, triggered the collapse of other large financial institutions such as AIG, Merrill Lynch and Washington Mutual. This generated a climate of panic in the financial markets and intensified the crisis.

Now: The American banking system does not operate in isolation. When a bank fails, a series of chain reactions can be triggered that affect other institutions and the financial system as a whole.

The failure of one bank can lead to a loss of confidence in the financial system, leading depositors to withdraw their money from other banks for fear that they may also fail.

This flight of deposits can leave other banks short of liquidity, making it difficult for them to meet their obligations and maintain operations.

Additionally, The failure of a bank can affect the economy as a whole, since banks play a crucial role in financial intermediation and in granting credit to companies and individuals. If at least one of the 63 banks that are currently in trouble fail, a cascade effect could be generated that makes access to credit more difficult, affects economic growth and generates an increase in unemployment.

3- Frozen credits

Before: In 2008, the financial crisis spread globally due to lack of liquidity in credit markets. Banks stopped lending money to each other and to consumers, causing a credit freeze and making it difficult for businesses and individuals to access financing.

Now: Rising interest rates are affecting demand for loans in the United States and putting banks, like New York Community Bank, in a difficult financial situation. Additionally, falling demand for office space due to remote work poses additional challenges for the banking industry.

The closure of the BTFP and the end of the emergency buffer in which lenders take refuge could make banks more cautious and less willing to take risks, which could lead to a liquidity crisis similar to that of 2008. Geopolitical tensions also pose an additional danger as they could increase risks.

Given all the challenges that the US banking system is going through, it is evident that the bankruptcy of a large group of banks is something that should be kept in mind for the remainder of the year.

However, it must also be taken into account that the US banking system is stronger now thanks to a series of measures and regulatory reforms that emerged after the 2008 crisis. Although, beyond that, massive bank failure is a possibility which has been underway for some time and will continue for the next few years.

Under the pressure of higher interest rates and operational problems, more than 50 US banks could fail. This was warned by Nomura analyst Greg Hertrich in May.

His analysis added at that time that high interest rates impact the banking system, but the reduction of these, will hit doubly hard on financial health of the lenders in that country.

Profits at smaller institutions could be squeezed if U.S. interest rates fall this year because banks will have to pay higher rates to customers to keep their money deposited in the accounts.

“Those deposits are expensive and there is concern about whether or not that funding will remain in a smaller institution once rates start to fall,” Hertrich said. His view is that falling rates could trigger capital outflows leading to bank failures.

There are currently more than 4,500 banks in the United States, government data showed, and this number is likely to be cut in half in the coming years.