The elderly surpass the young in wealth, money in the bank, income and home ownership

For years, younger families and those who are already retired or close to doing so have followed opposite paths in terms of their material well-being. Younger households are increasingly finding it more difficult to accumulate wealth. The consequences of the financial crisis have taken a heavy toll on their incomes, which have not stopped reducing, cutting off their access to the great train of wealth in Spain: bricks.

At the same time, their parents’ generation—now retired—has enjoyed more stable professional careers and has seen the real estate they purchased or inherited appreciate dramatically. The consequences are a gap between generations that continues to grow. Households whose head of family is over 65 years old accumulate more wealth, more money in the bank and generate more income than their counterparts under 35 years old.

This is the still photo you see when you observe how the economic well-being of different generations has evolved in the last 20 years. The portrait is carried out by the Bank of Spain through its Family Financial Survey (EFF), published last Monday.

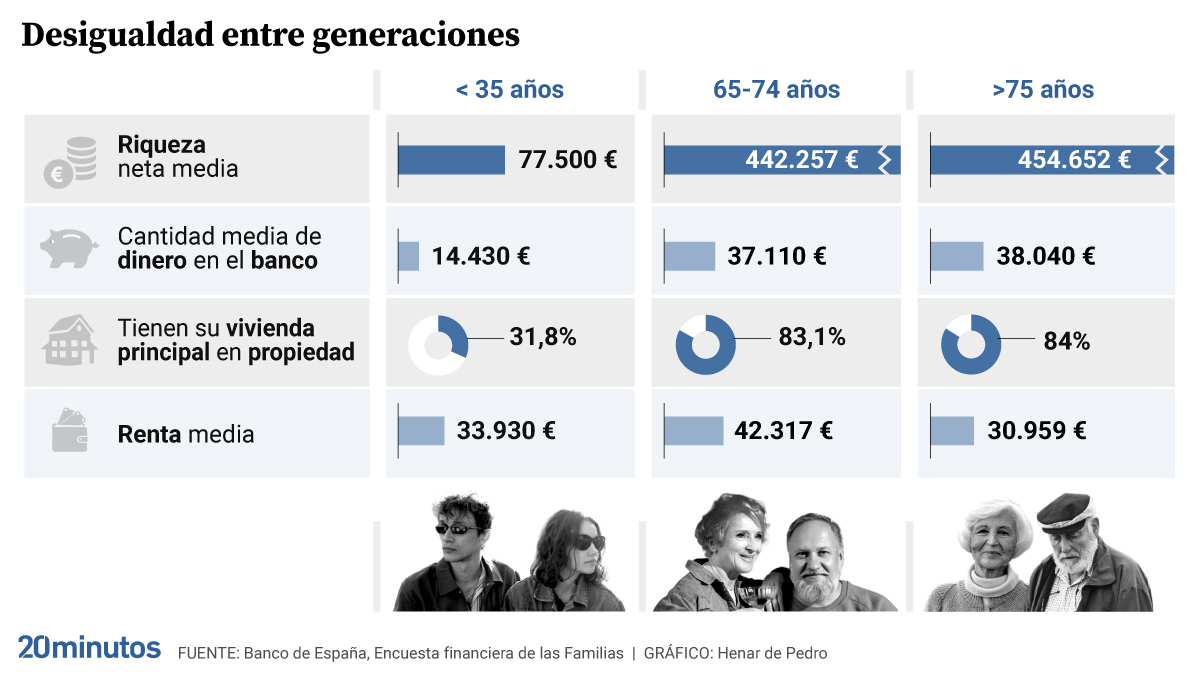

One of the most striking conclusions is the enormous gap that has opened between the wealth held by households whose heads of family are over 65 years old and those under 35 years old. In 2022, the wealth accumulated by older families amounted to an average of 442,257 euros, almost six times more than the younger generations, who barely have 77,500 euros of wealth on average. In fact, Half of families under 35 years of age have accumulated wealth that does not exceed 20,000 euros.

It is logical that older generations accumulate more wealth: throughout their lives they have had more time to generate savings that they have subsequently transformed into assets. However, The differences have widened dramatically in the last 20 years. In 2002, the wealth of families over 65 barely doubled that of those under 35.

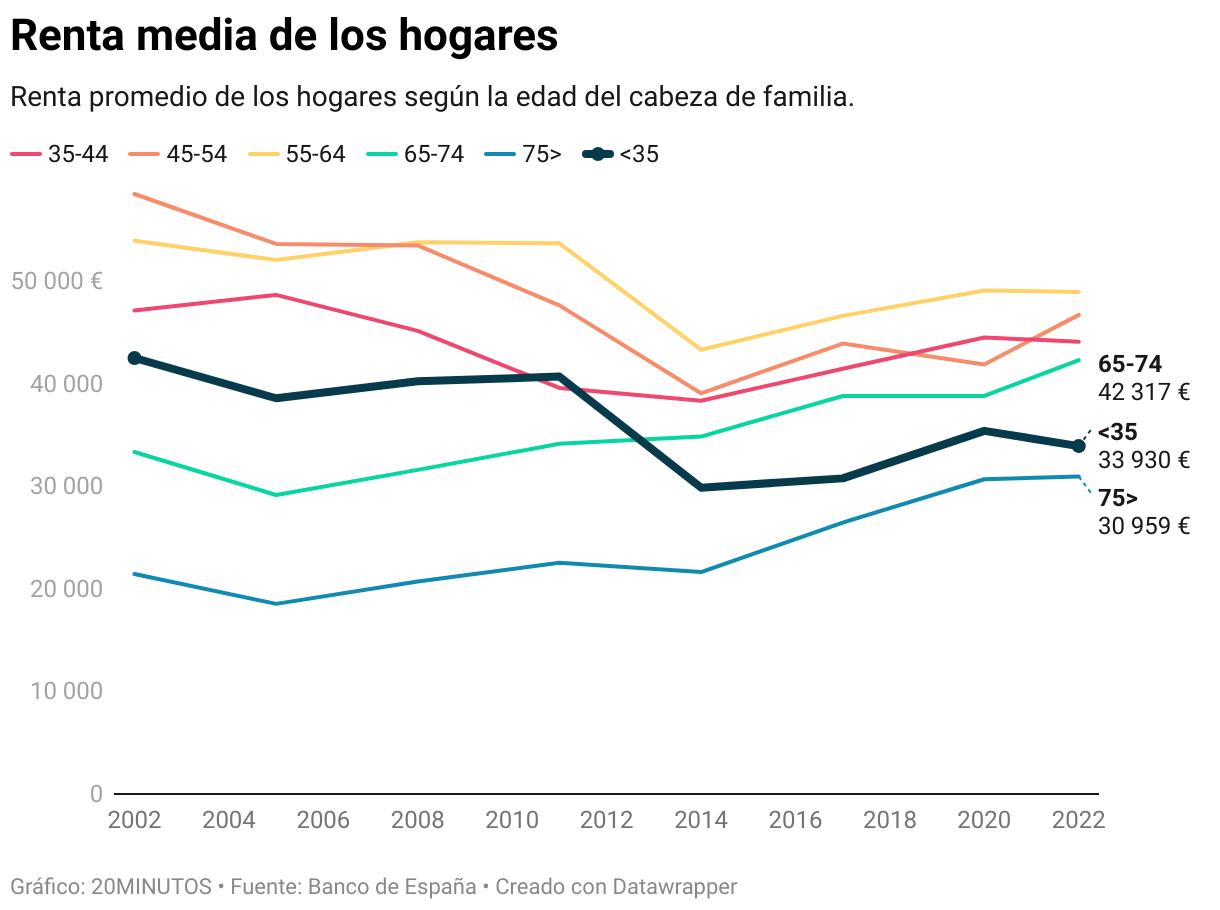

What has happened in between? The first is a financial crisis that has impoverished an entire generation that joined the labor market in one of the worst moments in Spain’s recent history. Compared to 2002, the income of younger families is now 20% lower: from 41,711 euros on average it has been reduced to 33,930. Furthermore, it must be taken into account that consumer prices were 50% higher in 2022 than twenty years ago, therefore, the purchasing power of those 42,000 euros in 2002 was much higher.

At the same time, The income of families over 65 years old is also higher now. In large part because people who are retiring these years have had longer working careers and have the right to receive more generous pensions. Furthermore, pensioners weathered the financial crisis better than young people. Pensions were frozen, but there were no cuts and in recent years the Government has protected its purchasing power.

50% of young people have less than €2,700 in the bank

This evolution has led to the paradox that the average income of families under 35 years of age (33,930 euros) is already very similar to that of those over 75 (30,959) and is below that of families between 65 and 74 years (42,317). This income situation is logically transferred to the bank account. On average, young people keep 14,000 euros in the bank, 61% less than those over 65 years of age. Besides, Half of families under 35 years old have 2,700 euros or less in the bank.

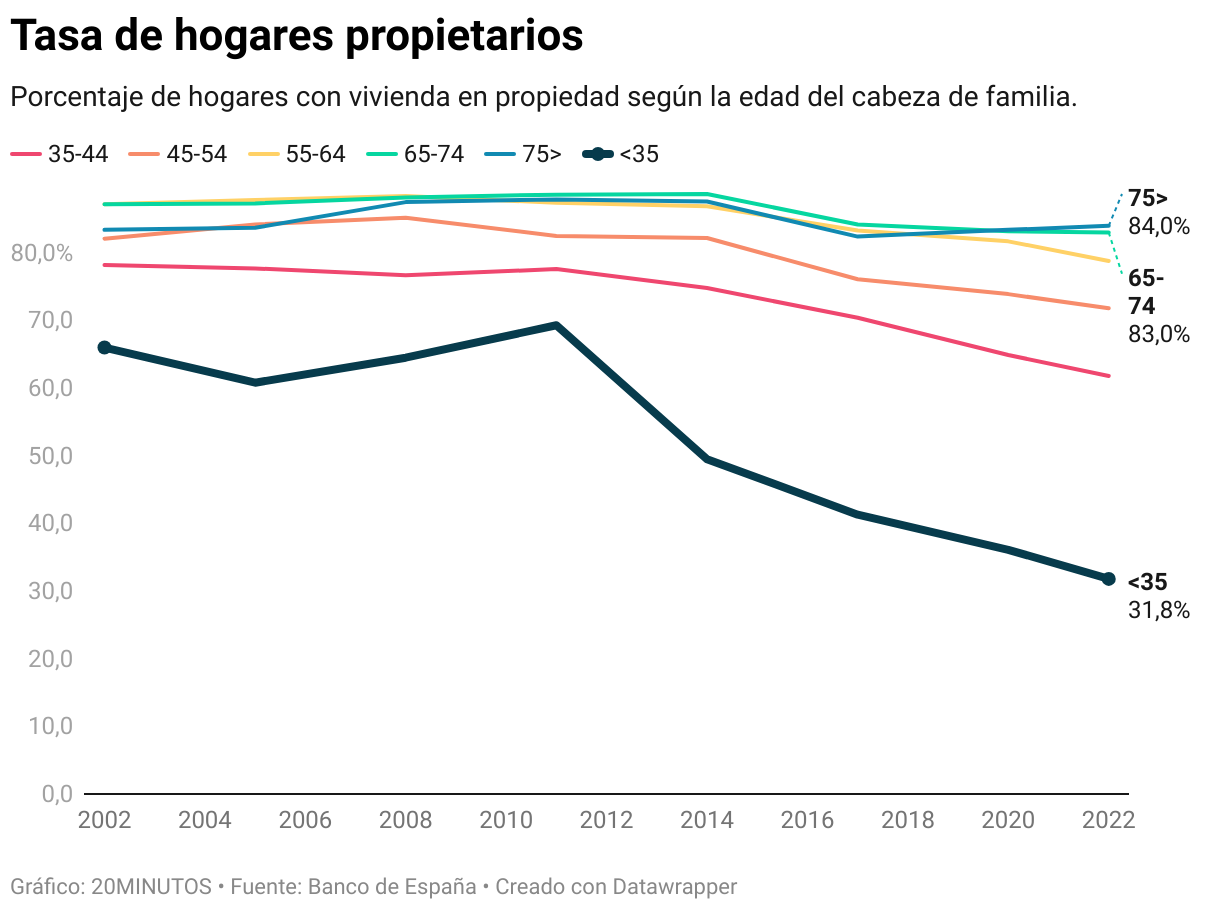

The sharp loss of income of young households has overlapped with housing prices that continue to rise and banks that are much more demanding when granting mortgages. These two factors have left many young households outside of the country’s main vehicle for generating wealth, which is home ownership.

The statistics are devastating. In 2002, two out of three households in which the head of the family was under 35 years of age owned a home. Twenty years later, the proportion was only 31.8%, while households over 65 years of age own their home in more than 83% of cases. At the moment, only 21% of young households have some type of mortgage debt linked to your main home.

“The accumulation of wealth is a reflection of how things have gone for you throughout your life, it is what you have been able to save from your income,” explains José Ignacio Conde-Ruiz, researcher at Fedea and author of the book The docked youthin conversation with 20 minutes. For this specialist, the solution to the problem is to allocate more public resources to young people, something that will not be cheap. “Measures are necessary, it is a first-level problem that we are going to have to face. We must invest resources and prioritize the well-being of young people,” he maintains.

“Young people are being left behind. It is not just a problem of access to housing. If there was a stable job market or high salaries I wouldn’t worry, but that’s not the case. With wealth, more of the same happens, there is hardly any support for youth, emancipation, having children…”, he adds.

The catch-all of pensions

As with any generalization, the better financial situation of the elderly lends itself to qualifications. Although older households accumulate more assets and increasingly more income, the situation of retirees is very heterogeneous. There is an important group with high benefits, but half of retirement pensions did not reach the minimum wage in 2023.