Will the dollar explode soon or not? Lyn Alden analyzes debt risks

-

Many Bitcoiners predict a soon collapse of the US currency.

-

There are those who “benefit from sensationalism,” says Alden.

The possibility of an imminent collapse of the US dollar generates debate in financial markets. Many Bitcoiners repeat this idea and even yearn for that way, because that – in theory – would be beneficial for Bitcoin (BTC).

But, the financial specialist, Lyn Alden. He maintains that an abrupt crisis is unlikely. Instead, it raises a stage of progressive deterioration.

Alden comments that many extreme forecasts arise from incomplete media incentives and that A part of those who predict a nearby collapse “benefit from sensationalism”while others simply misunderstand the current macroeconomic dynamics.

Several Bitcoin enthusiasts, for example, anticipate a monetary collapse as a direct consequence of the increase in a public debt crisis and fiscal deficits. In fact, they see that scenario as a potential catalyst for the price of digital asset, as reported by cryptoics.

Nevertheless, That perspective omits key structural factorsaccording to Alden.

One of these factors is that the United States currently records a fiscal deficit equivalent to 7% of its GDP, equivalent to just over 1.4 billion dollars so far. While this figure is high, remains far from extreme levels. The problem is structural and difficult to reverse, says the analyst, but not unsustainable in the short term.

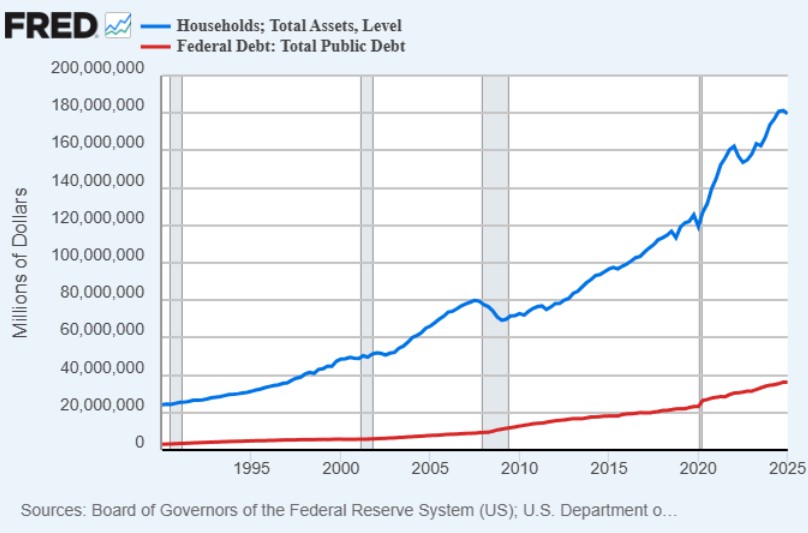

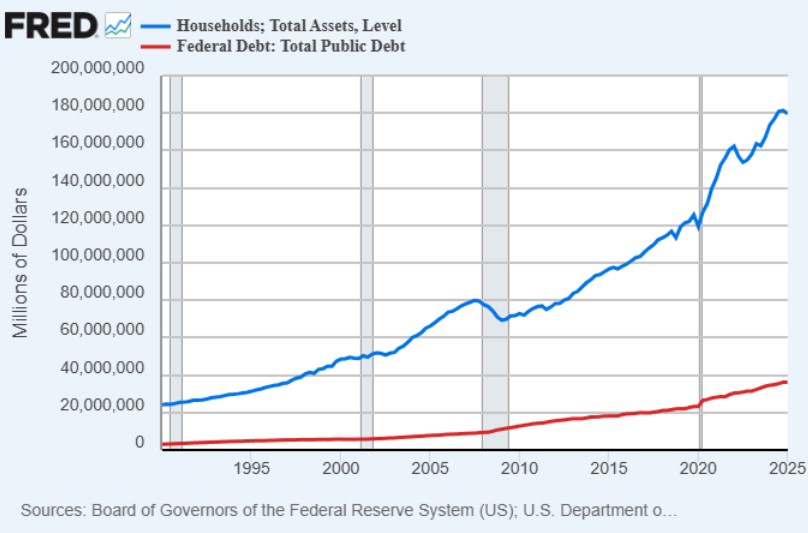

Likewise, the Federal Government has a debt of more than 36 billion dollars. Although that number seems alarming, it cannot be analyzed in isolation. American households have about 180 billion dollars in assets and around 160 billion in net worth after deducting liabilities, as seen in this graph:

Alden explains that, although it is not a direct comparison between public debt and private wealth, It serves to dimension the relative magnitude of both amounts.

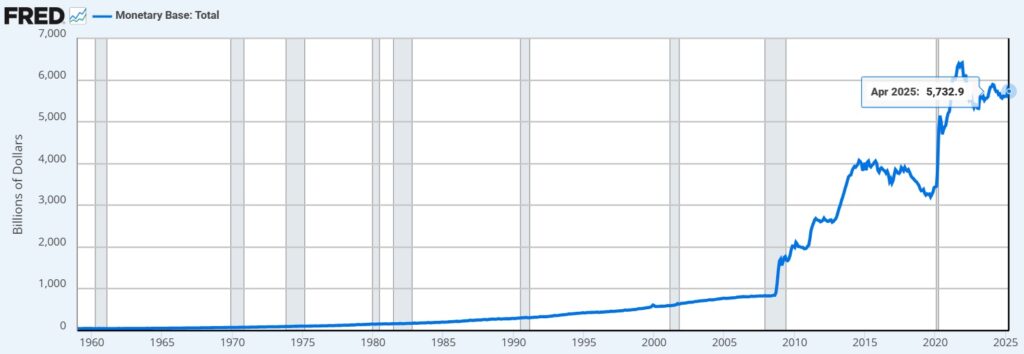

Even more relevant is the global monetary dynamics. The US monetary base is around 6 billion dollars, as seen in the following graph, while the total debt and loans called in dollars – at national and international level – exceeds 120 billion.

Of that total, About 18 billion correspond to external debtthat is, contractual commitments outside the US. This implies that a large number of economic agents around the world need dollars. And it is that structural and inflexible demand that limits the risk of abrupt depreciation of the green ticket, the analyst considers.

Unlike countries such as Venezuela, Argentina or Türkiye, whose currency lacks international demand, the dollar operates within a global financial network where multiple agents – which should not be mutually – They are obliged to comply with payments in dollars.

This generates a constant pressure acquisition pressure that does not disappear even if the money supply increases. Therefore, Alden argues, even if the monetary base doubles or triples, That does not automatically flow into hyperinflation. The amount of contractual demand absorbs much of the increase.

It is not a harmless situation

Now, this does not imply that the situation is harmless. US fiscal policy It already affects the federal reserve capacity To control credit growth, says the specialist.

According to Alden, the system operates in a state of “fiscal dominance”, where the need to maintain the liquid and functional treasure market limits monetary autonomy. That is, the Fed can Be forced to intervene to avoid disruptionseven at the cost of tolerating inflation.

Events such as the United Kingdom’s bond crisis in 2022 show what could happen. In stress contexts, the Central Bank It can intervene with measures such as quantitative flexibility.

This usually stabilizes the system in the short term, but has inflationary costs, because it implies a greater monetary impression, which can distort assets prices. In any case, it does not generate a total dollar crisis.

In that order of ideas, future evolution, according to Alden, is more similar to A slow -chamber train than to a sudden explosion. The current deficits are difficult to reverse, and the combination of increasing debt, monetary intervention and external demand of the dollar draws a scenario where risks increase over time. There is no defined breakdown. The situation gradually aggravates.

Alden states that it is more useful to think about fiscal dynamics as a dial that is turning, not as a switch. The problem is already present, but it can be extended for years without implying an immediate collapse.

“The deficits are more intractable than the bulls think, which means that it is very unlikely that the Federal Government of the United States will control them in the short term. But, on the other hand, it is not as imminent as the bassists think; it is unlikely that it causes a total crisis of the dollar in the short term. It is a crash of trains in a very long slow chamber. A dial that turns little by little.

Lyn Alden, financial analyst.

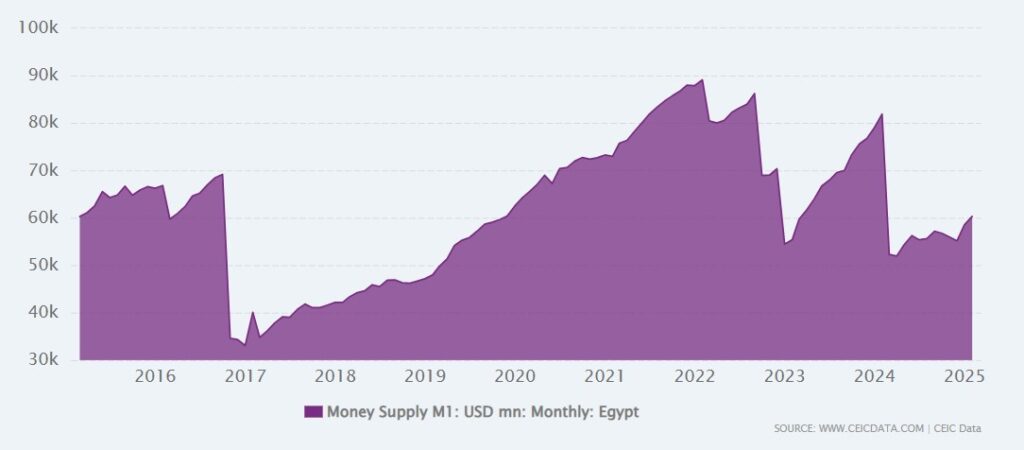

Recent history shows that other countries have endured high levels of monetary degradation Without reaching the total collapse. Egypt, for example, multiplied for more than six its money supply in a decade, as seen in the following graph, which led to a significant depreciation of its currency, but not to a system stoppage.

In other economies, such as China, Brazil or India, the growth of the money supply has also been higher than in the US China reached 145% in the last decade; Brazil, 131%; India, 183%. But none of these currencies has completely collapsed. According to Alden, this shows that The devaluation can be extensive and sustained without reaching absolute collapse.

The dollar faces structural challenges derived from indebtedness and deficits. However, its status as a global reserve currency and the inflexible demand that generate protects it from a sudden crisis. The risks around that currency accumulate slowly and can last decades to feel, according to Alden’s estimate.

The interesting thing is that, in that interim, Bitcoin takes spaces and profiling himself as a real reserve asset, removing that place to a dollar that, although slowly, is constantly devalued.