Can the XRP and Solana ETFs avoid the fate of those of Ethereum?

The United States Stock Exchange and Securities Commission (SEC) currently has more than 70 applications on the table to launch funds quoted in the Bag (ETF) of cryptocurrencies.

This “fever” for launching ETF unleashed after the departure of Gary Gensler, former president of the SEC. Since then, Companies have proposed Listar ETF that include from Altcoins consolidated and “serious” as Solana (Sol) or XRP, even memecoins such as Dogecoin (Doge).

This impulse also responds to the new favorable climate for cryptocurrencies that was generated with the arrival of Donald Trump to the White House.

As cryptootics reported, throughout its presidential campaign, Trump expressed a position in favor of the sector and promised to create a friendly regulatory framework to promote industry growth.

And, so far, it is complying with some of those promises such as the decision to create a cryptocurrency advisory council or appoint Paul Atkins at the head of the SEC, who will assume that function as of June 5 and was praised by Trump to recognize that the “digital assets and other innovations are key to making the United States a better country”.

Given this scenario, coin investors such as XRP, Solana or Litecoin (LTC), among others, They rub their hands and look forward to these ETFs to leave the market as soon as possible.

However, an interesting issue follows here: ETF al Caé de Ether (ETH), Ethereum’s native cryptocurrency, have had a much lower performance if compared to those of Bitcoin (BTC).

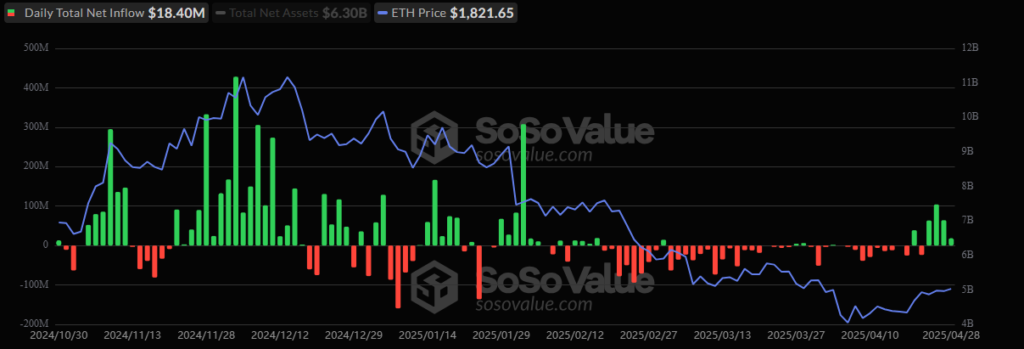

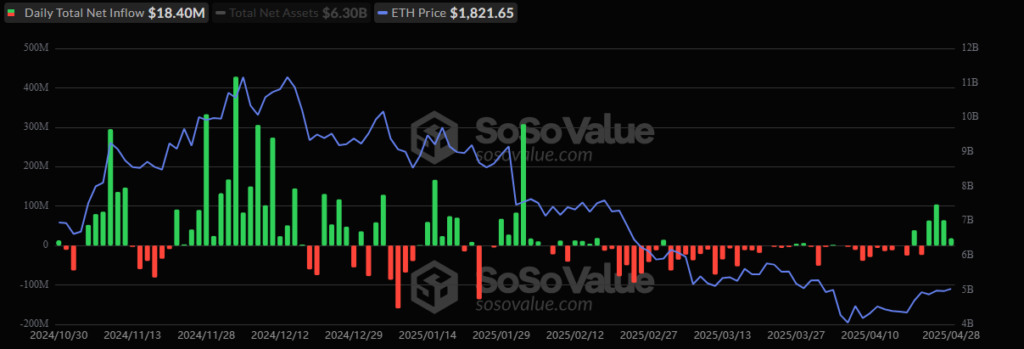

Since its launch in July 2024, ETH financial instruments record money tickets for 2,480 million dollars and, as seen in the following image, they have not had a positive impact on its price (blue line).

At the time of its debut, ETH quoted at $ 2,510. Today, its price is $ 1,800.

That said, the following question remains to be raised: Why do Altcoins insist with the ETFs if Ether did not rise in price?

In this regard, Eric Balchunas, analyst of Bloomberg Intelligence, He said: “That your currency becomes ETF is like being in a band and that your songs are added to all music streaming services. It does not guarantee that they listen to them, but place your music where the vast majority of listeners are”

That is, if a digital asset has its own ETF will have more exposure between institutional investors and broad adoption through the managers of these funds. If they succeed, this will generate an upward impulse in their quotation.

Otherwise, what is happening with ETH funds could happen.

To answer the question above, analysts from The Token Dispatch site indicate the difficulties faced by financial instruments based on Ethereum’s native currency such as high commissions.

The Grayscale Ethereum Trust (ETHE), for example, has a commission of 2.5%, makes it recently competitive against cheaper options such as Blackrock (0.25%).

Another issue is that the value proposition is too complex compared to the BTC narrative as “digital gold”, which makes adoption between advisors and investors.

“Ethereum’s value proposal covers being an intelligent contract platform, a liquidation layer for Defi, a spine of the NFT market and, potentially, an asset generator of performance by staffing, a feature not available in current ETF ETFs,” explain the analysts.

For this reason, they consider that “this complexity creates a marketing challenge”, and highlight: “When financial advisors cannot easily explain an investment thesis to customers in one or two phrases, adoption is affected. Bitcoin’s simplicity won that battle farmer.”

They also warn that the fact that these instruments do not allow staking is an obstacle, A feature that differentiates ETH from Bitcoin.

As cryptootics, companies such as Grayscale, 21Shares and Fidelity have reported, have submitted applications to the SEC to incorporate the staffing into their ETH financial instruments.

Staking, which consists of depositing ETH in intelligent contracts in exchange for rewards, could be the next great step for these funds.

The interesting thing for the analysts of The Token Dispatch is: “The catalyst is to recognize that ETH ETFs failed not because they are ETF, but because they are bad substitutes for the native ETH. When comparing the 2.5% commission of ETHE and the zero profitability of the staking with the simple possession of ETH, the decision becomes mathematically obvious.”

In other words, ETHher’s ETFs could become The “sacrificial pioneer” that opens the way to a second more successful wave. In addition, they say:

“The failures of current ETH ETFs will not demonstrate that the cryptocurrency ETFs do not work; they will, however, the essential feedback of the market that will make the next generation work better.”

The Token Dispatch site analysts.

So … why bet on the launch of ETF of other cryptocurrencies?

Although an ETF is not a guarantee of price increases for the underlying asset, The enthusiasm for launching similar products based on Altcoins does not show signs of cooling.

This paradox responds to a series of factors that, for many emitters, weigh more than the warning signs left by the ETH case.

According to a Coinbase and EY-Parthenon report, about 83% of institutional investors plan to increase their assignments to cryptocurrencies this year, and many point to more than 5% of assets under management.

In this regard, The Token Dispatch specialists argue that “each Altcoin also offers differentiated value proposals that could resonate more clearly than Ethereum’s complex narrative.”

These proposals include the “ultra -grape” speed of transactions in the Solana network and the XRP approach, which seeks to position itself as “the cryptocurrency of the banks”, although its adoption in the banking sector remains limited.

Another issue that must be taken into account is the potential growth of cryptocurrencies that have a lower market capitalization.

“While BTC and ETH can offer stability, their market capitalizations of one billion dollars limit their bullish potential. Medium capitalization altcoins could generate more significant yields if they achieve widespread adoption, which could attract investors focused on growth that lost the initial profits of BTC,” the specialists highlight.

In addition, JP Morgan analysts project that Solana ETFs could attract 3,000 and 6,000 million dollars in their first yearwhile those of XRP would capture between 4,000 and 8,000 million dollars.

With these arguments, we can return to the question of the title: Could the XRP and Solana ETFs avoid the fate of ETH? The answer is yes.

Mainly because, if JP Morgan’s projections are met, these products could generate a much stronger impact on the prices and market dynamics than the ETF of Ether had.

This is because, due to the very structure of the ETFs, the issuing companies are obliged to acquire the underlying asset to support their funds properly.

Consequently, if the demand grows, these firms must go to the market to buy, which, for a basic issue of supply and demand, usually press the rising price.

We will have to wait to see what happens with the ETFs of XRP, Sol and other Altcoins. The truth is that, despite the fact that the most recent antecedent is not encouraging, investor enthusiasm does not stop growing.

Meanwhile, the SEC still does not offer a clear response to the avalanche of applications on the table.

Discharge of responsibility: The views and opinions expressed in this article belong to its author and do not necessarily reflect those of cryptootics. The author’s opinion is informatively and under no circumstances constitutes an investment recommendation or financial advice.