requirements, deadlines and how to apply

Buy a house It is an almost impossible mission for millions of young people in Spain: The average price per square meter is 2,098 euros, close to the all-time high and almost 7 points above the price from a year ago, according to Idealista data. In that sense, the guarantees from the Official Credit Institute (ICO) Announced by the Government last February, they intend to promote the purchase of housing in this sector of the population.

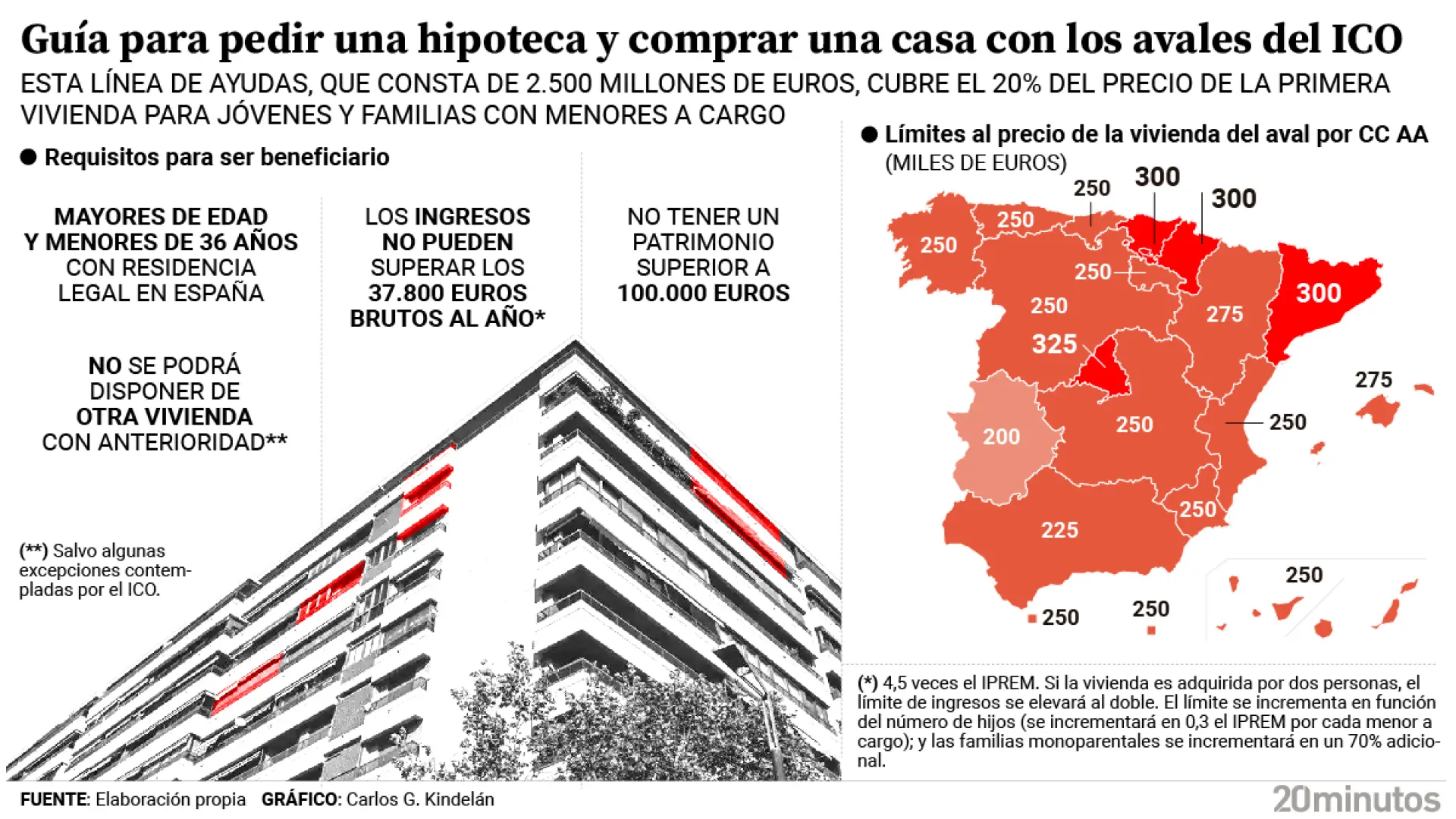

This aid line, which consists of 2.5 billion euros, covers 20% of the price of the first home for young people and families with dependent minors. With these guarantees, beneficiaries can pay the down payment for the purchase of the home, that 20% that banks normally require to sign a mortgage, according to the official ICO website.

Access to this line of ICO guarantees must be requested through the banks that have joined the initiativeand the path to request it is marked by compliance with a series of requirements, deadlines and necessary documents.

Who can request ICO guarantees? These are the requirements

In general, these aids are aimed at young people up to 35 years old and families with dependent minors. The guarantees cover up to 20% of the amount of the home, with maximum limits established in the BOE on the price of said home. If the purchased home has an energy rating of D or higher, up to 25% of the amount may be guaranteed.

The granting of ICO guarantees is subject to compliance with a series of requirements:

- The beneficiaries must be of legal age and minors under 36 years of age, with legal residence in Spain (being able to prove it for at least two years prior to the loan application).

- The person requesting the endorsement You cannot have assets greater than 100,000 euros.

- The income From applicant They cannot exceed 37,800 euros gross per year (4.5 times the IPREM). In the event that the home is purchased by two people, the income limit will be doubled (that is, the income of both cannot exceed the sum of both limits). The limit increases depending on the number of children (the IPREM will increase by 0.3 for each dependent minor); and single-parent families will increase by an additional 70%.

- The appliers They will not be able to have another home beforehandexcept for some exceptions contemplated by the ICO.

- The guarantee can be maintained within the established limitsas long as it is the beneficiary’s habitual residence.

In which banks can I request mortgages with the ICO guarantee?

Until 29 entities have joined this line of ICO guarantees, so through them contracts can be formalized that include these first home aid for young people and dependent families:

- Santander Bank

- BBVA

- Ibercaja Bank

- Evo Bank

- Ontinyent Savings Bank and MP

- Arquia Bank

- UCI, Union of Real Estate Credits SA

- Almendralejo Rural Bank

- Abanca Banking Corporation

- Spanish Cooperative Bank

- Cajasiete, Rural Bank

- Caja Rural de Extremadura

- Soria Rural Bank

- Teruel Rural Bank

- Caja Rural del Sur

- Granada Rural Bank

- Salamanca Rural Bank

- Caja Rural de Utrera

- Caja Rural San José de Alcora

- Caja Rural de Jaén, Barcelona and Madrid

- Zamora Rural Bank

- Caixa Rural Galega

- Regional Rural Bank

- Caja Rural de Cañete de las Torres

- Gijón Rural Bank

- Caixa La Vall S.Isidro

- Caixa Popular

- Caja Rural de Nueva Carteya

- Caja Rural de Aragón

The documents you must present to request the guarantee

The BOE establishes the documentation which will be required with the request for endorsement as accreditation of compliance with the requirements. Of these documents, declarations and certificates, which must be provided to the banking entities, the following stand out:

- IDNIE or passport of all home buyers.

- IDNIE or passport of the minors in chargefamily book or document proving registration as a de facto couple if applicable.

- Census municipal coexistence certificate to prove residence in Spain.

- Responsible statements of the Client who certifies that the financed home is intended for habitual and permanent residence; and that proves that the home is not used for the exercise of an economic activity.

- Negative cadastral certificate that proves that none of the purchasers is already the owner.

- Contract purchase and sale of housing.

- Energy certificate issued on a date prior to or equal to the date of purchase of the home.

- Report appraisal of the financed home carried out for the purposes of contracting the mortgage loan.

- Authorization to the ICO signed by the Clients to consult their CIRBE data throughout the life of the guaranteed loan.

- Last personal income tax return or, if there is no obligation to present it, a negative certificate from the AEAT. Authorization to MIVAU signed by the Clients to consult their Tax Agency data throughout the life of the guaranteed loan.

- Responsible declaration of the Client’s compliance with the assumptions of article 13 of the General Subsidies Law.

There are limits to the price of the guarantee home

The BOE establishes, in turn, the maximum price of the home, after which guarantee is no longer offered. These thresholds are set depending on the Autonomous Community and range between 325,000 euros in the Community of Madrid and 200,000 euros in Extremadura.

- Andalusia: 225,000 euros.

- Aragon: 275,000 euros.

- Asturias: 250,000 euros.

- Balearic Islands: 275,000 euros.

- Canary Islands: 250,000 euros.

- Cantabria: 250,000 euros.

- Castilla y León: 250,000 euros.

- Castilla-La Mancha: 250,000 euros.

- Catalonia: 300,000 euros.

- Valencian Community: 250,000 euros.

- Extremadura: 200,000 euros.

- Galicia: 250,000 euros. Madrid: 325,000 euros.

- Murcia: 250,000 euros.

- Navarra: 300,000 euros.

- Basque Country: 300,000 euros.

- La Rioja: 250,000 euros.

- Ceuta: 250,000 euros.

- Melilla: 250,000 euros.

How to request ICO guarantees step by step

After knowing and taking into account the requirements, analyze and design a budget to purchase the home with the guarantee, to be able to access these ICO aids simply You must go to one of the entities attached to the program to start the process, which will be the same as signing a mortgage.

It must be provide the entity with all required documentation that proves the requirements and that is requested to access the line of guarantees. The bank assigned to the program will begin the procedures for the signing of the mortgage with the financing of the ICO guarantee, as explained by the specialized portal Fotocasa.

Until when can you request?

According to the ICO, the deadline to formalize the loans that qualify for this line of guarantees ends on December 31, 2025. The Administration clarifies that the term of the guarantee is “a maximum of 10 years from the date the operation is formalized, regardless of the amortization of the loan.” During this period, the home must be the habitual residence of the guaranteed person.