The ECB begins an uncertain phase of rate cuts, but mortgages will not be as cheap as before inflation

The times of interest rates at historic highs and prohibitive mortgages are beginning to come to an end in Europe. However, The road seems long, uncertain and with an arrival point that will not be very similar to the departure point.. This will be especially noticeable to those with variable rate mortgages, whose monthly payment will no longer be what it was before the crisis. The European Central Bank (ECB) approved on Thursday the first drop in official euro interest rates since it began raising them almost two years ago to try to curb inflation.

With prices increasingly controlled (the eurozone CPI rose to 2.6% in May), The battle against inflation is approaching its end. However, the ECB is reluctant to bury the hatchet. Although prices are already very close to the central bank’s target, the euro supervisor has some concerns in mind. Specifically, he worries about what the ECB calls “domestic” inflation, that is, that which affects goods and services produced within the eurozone.

These prices are closely linked to salaries, which are still rising to historically high levels in the euro countries. In the first quarter, salary increases negotiated in agreements accelerated to 4.7% year-on-year. The ECB has said on different occasions that it closely monitors this metric when making its decisions. However, its economists believe that the increases will moderate throughout the year.

The president of the central bank, Christine Lagarde, insisted in the press conference after the announcement that the ECB is not committed to any predefined path of lowering rates. They will evaluate the situation meeting by meeting and make decisions based on the data that is arriving. This makes analysts who follow the ECB news think that a rate cut at the next meeting scheduled for July 18 is unlikely. The markets are currently betting that the ECB will lower rates at least once more in the remainder of the year. And they believe that it is likely that a second decline will also occur before 2025, although in this case they do not take it for granted.

any time passed was better

The pace at which interest rates are reduced worries, of course, those with variable rate mortgages or people who are waiting for the best time to apply for a loan. The faster and more decisive the fall, the faster and more intense the relief will be. for those who have a variable loan. And the conditions that those who want to access credit will be able to find are better.

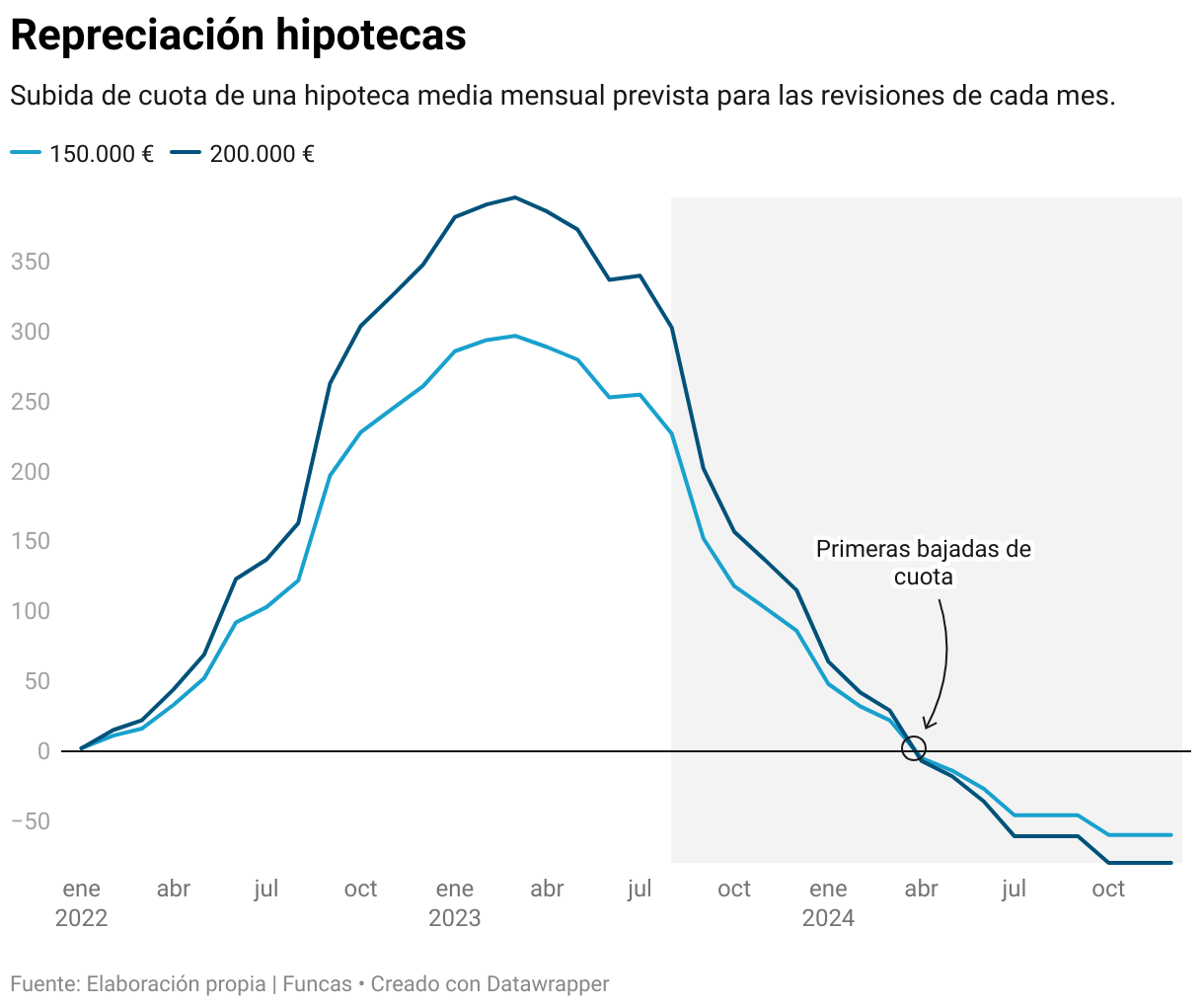

This is because the Euribor – the indicator that determines how much the vast majority of variable rate mortgage holders have to pay per month – fluctuates hand in hand with the interest rates set by the ECB. When these fall or are expected to fall, the Euribor usually falls as well. The lack of certainty about what will happen with medium-term rates has caused The Euribor has been stuck at around 3.7% for months without showing any signs of a decided decline.

The consensus of the analysts included in the Funcas panel suggests that the Euribor will still be around 3.2% in December of this year. If we accept the path anticipated by this panel, in the coming months There will be reductions in monthly mortgage payments of up to 9.1%which would translate into 81 euros per month of savings for an average mortgage (150,000 euros for 25 years, with an annual review and a differential of one point over the Euribor).

However, it does not seem that the relief will ever be enough to compensate for all that mortgages have become more expensive since the end of 2022. The longer-term forecasts place the Euribor at around 2.76% at the end of 2025. If this scenario were to materialize, the average mortgage would be in December of next year up to 45.2% more expensive than it was before the ECB started the current cycle of types. For an average loan we would be talking about 240 euros more per month.

The end of the journey

But the big question that opens up with this new phase inaugurated on Thursday by the ECB is where the ground is. What will be the level at which interest rates will stabilize. The uncertainty on this issue is enormous. Professional analysts surveyed by the ECB believe that The final goal could be an interest rate between 2 and 2.5% for long-term deposits (currently the level is 3.75%).

However, it does not seem that this is the ECB’s main concern right now. “We know the destination. We know the direction we are taking. We know the methodology we will apply (…) but what “It’s very uncertain is the speed at which we travel and how long it will take.”Lagarde concluded.