This is how the mortgages that will be reviewed will look like

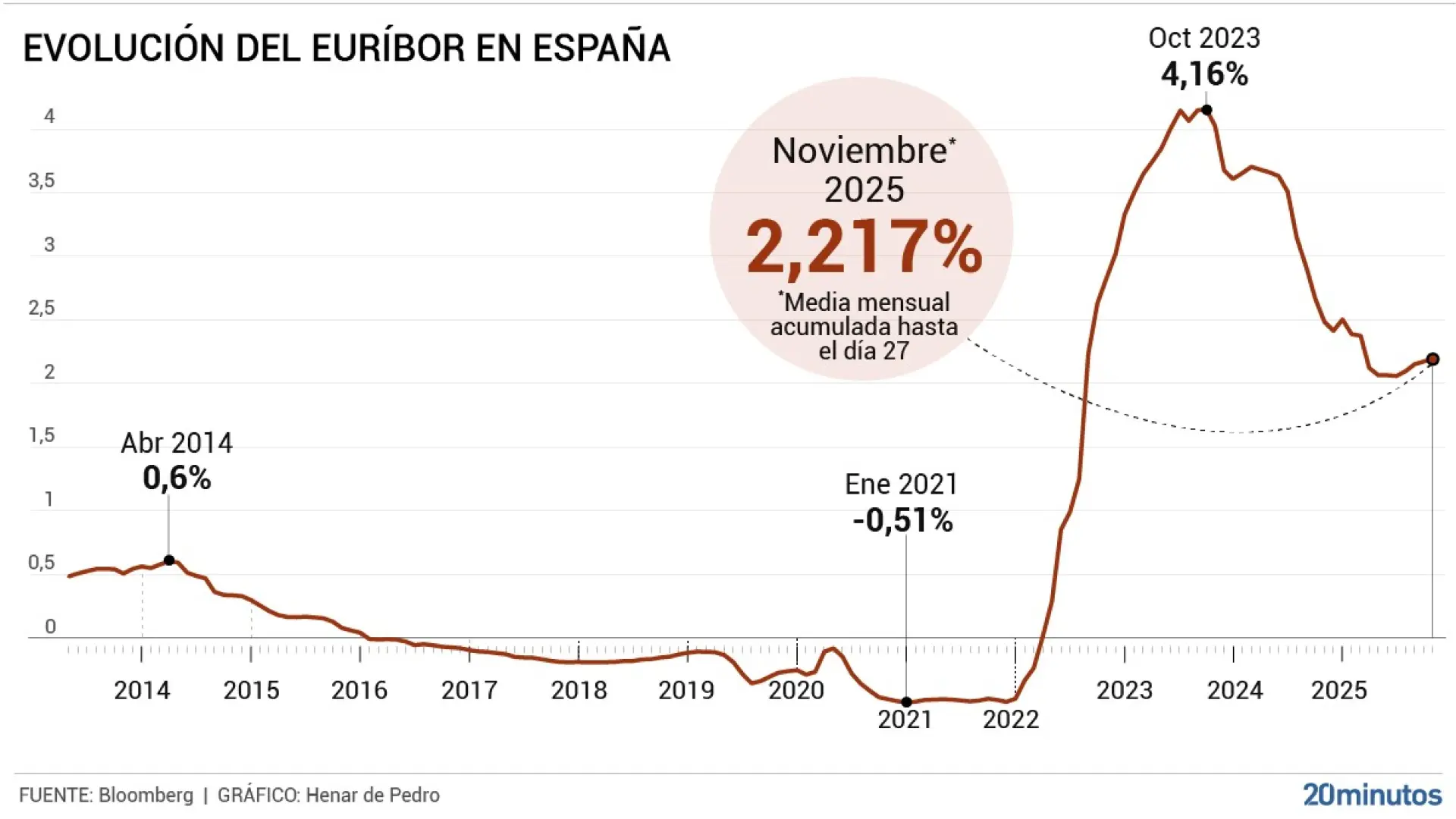

He euriborthe reference indicator in Spain to calculate variable mortgages, will close again with all probability upwards in the month of Novemberthus adding its fourth consecutive increase after chaining decreases between January and July in line with the rate reduction policy carried out by the European Central Bank (ECB). In this way, in the absence of knowing the final data for the end of the month this Friday, its average rate is provisionally above 2.2%.

The consequence of this increase will be suffered by those variable mortgages that undergo a semiannual review with the November data. So, for a loan of about 150,000 euros for 25 years with an interest rate of Euribor and a spread of 1%, The fee will increase around 130 euros per year. In the case of a higher mortgage, of 300,000 euros, with the same characteristics as the previous one, the increase will be about 265 euros per year.

Instead, Variable mortgages with annual review will continue to register a reduction in installmentsalthough to a lesser extent than in previous months. This is because a year ago, in November 2024, the Euribor closed at 2.506%, a rate higher than the current rate. This way, in the case of a mortgage of 150,000 euroswith the same characteristics as the previous one, the savings will be about 276 euros per year, while in a loan of 300,000 euros it will reach about 516 euros.

During this month of November, the Euribor has oscillated between its maximum daily rate, which marked on the 14th, at 2.235%, and the minimum, 2.199%on November 3rd.

Various analysts explain that the upward movements in the mortgage index are motivated by the ECB decisions which, at its last meeting last October, chose by keep interest rates unchanged at 2%, and foresee few fluctuations in the coming months. In addition, they highlight that for mortgages with annual review the fee will still continue to decrease. The next meeting of the European issuer will be held on December 18.

According to Michael Rierafinancial comparator analyst HelpMyCashwe find ourselves facing a new cycle because the situation of the mortgage indicator has changed in this last part of the year, although “there should be no panic”. The latest increases in this index respond to a “normalization process”in his opinion, which is explained by the different movements that the European banking regulator has carried out. Looking ahead to the coming months, forecasts suggest that the ECB will keep its rates frozen. For this reason, HelpMyCash predicts thatThe Euribor will remain relatively stable until the end of the year and during the first half of 2026; without abrupt drops or disproportionate increases.

“The normal thing is to end the year around 2-2.2%”

The Abante fund selector, Alvaro de la Rosafor his part, recalled in statements to Efe that the indicator had been “more stopped” for a few monthsin line with the ECB’s messages, and estimated that, taking into account that expectations are that rates will remain flat between now and the end of the year, what can be expected is that the Euribor will not register large movements in the coming quarters. “If we do not see these movements on the part of the ECB, the normal thing is that we could end up in an environment of 2-2.2%”estimated the expert.

The Euribor represents the interest rate at which European banks lend money to each other, with a maturity period of 12 months. This indicator plays a crucial role in the calculation of variable mortgages and is published in different terms: 1 week, 1 month, 3 months, 6 months and 12 months. The interest on variable mortgages in Spain is reviewed semiannually or annually, depending on what appears in each contract.